Cyber Insurance

Built to defend your clients against evolving cyber threats, with security to help prevent incidents and coverage to protect them when it counts.

Cyber Coverage Highlights

Direct and Contingent coverage for Business Interruption and System Failure

Social Engineering & Invoice Manipulation coverage available for all classes of business

Full limits offered for Cryptojacking and Bricking coverage

Broad Cyber Extortion coverage including payment of cryptocurrencies

Reputational Harm coverage including PR costs as a result of Adverse Publications

Ability to manuscript endorsements to address specific exposures

Comprehensive Information Privacy coverage includes the unintended violation of any Privacy Regulation, including GDPR & CCPA

Access to At-Bay Stance, your client’s unified security platform, is included with every policy1

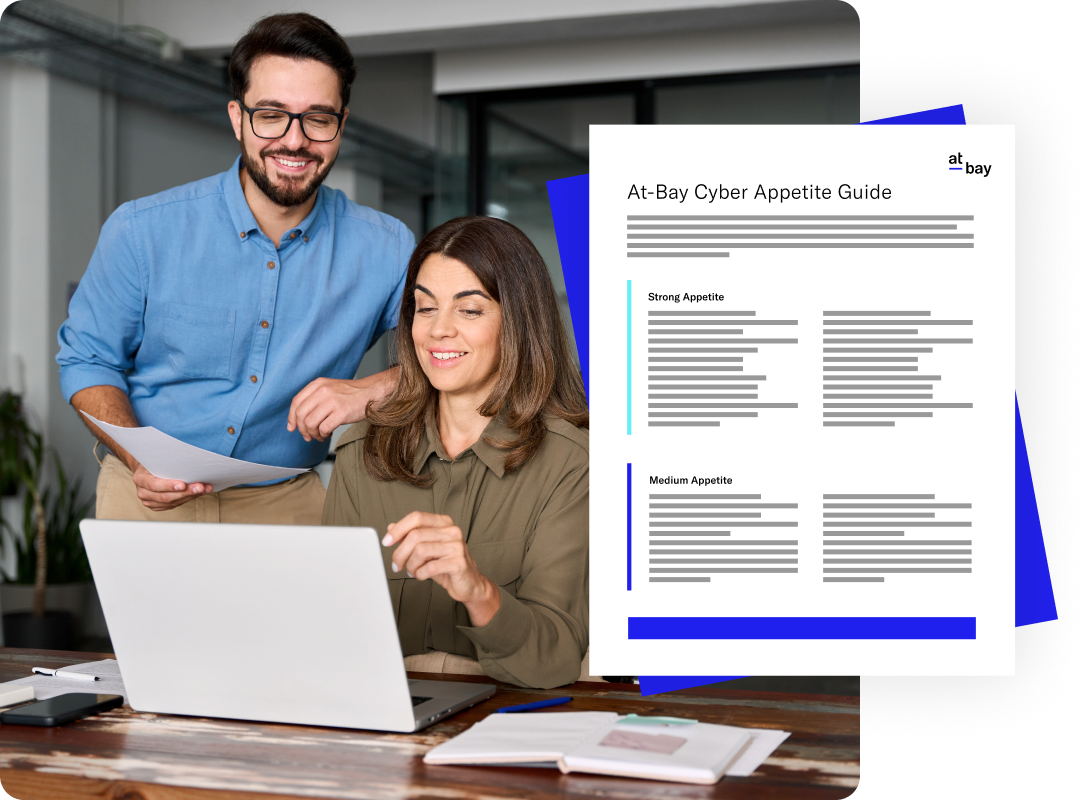

Primary & Excess Appetite

At-Bay provides cyber insurance on a primary and excess basis for businesses with up to $5 billion in revenue with limits up to $10 million.

Through our Broker Platform, brokers can get quotes in seconds for businesses with up to $100 million in revenue with limits up to $3 million.

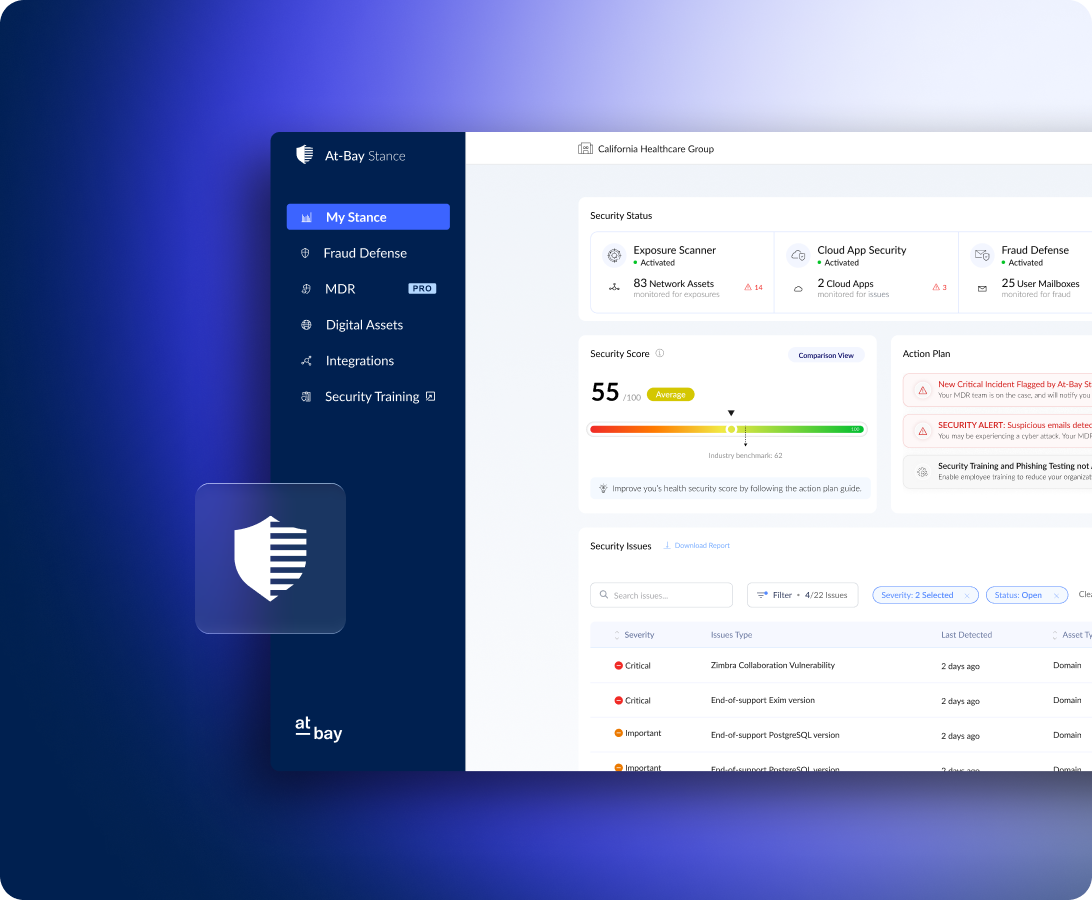

At-Bay Stance

Access to At-Bay Stance is included with every Cyber policy — a unified security solution valued that 1 in 3 policyholders actively use to reduce their cyber risk.1

What’s Your Cyber Risk?

Quickly determine your client's financial exposure to cyber attack with our cyber risk calculators.

INSURSEC PACKAGES FOR AT-BAY

Unlock Enhanced Coverage to Protect Against Ransomware and Financial Fraud

Better security. Better coverage. Better outcomes. That’s InsurSec.

Send us your submissions

Email your submissions to underwriting@at-bay.com or get automatic quotes on At-Bay's Broker Platform.